|

|

|

|

|

|

|

|

Medical

care means amounts paid for the diagnosis,

cure, mitigation, treatment, or prevention

of disease, and for treatments affecting

any part or function of the body. The

medical care expenses must be primarily

to alleviate or prevent a physical or

mental defect or illness. The following

provides details to special issues related

to medical care expenses. However, keep

in mind, there are income

restrictions limiting the medical

deductions.

|

A popular website for medical information

is WebMD.

|

|

|

|

Limitations

Restricting Medical Deductions

There are basically two limitations restricting

a deduction for medical expenses.

|

You must itemize your deduction,

and

|

|

You can deduct only the amount

of your medical and dental expenses

that is more than 7.5% of your adjusted

gross income. If, for example, your

only income for the year was $50,000

from wages and there were no adjustment

to your income, your adjusted gross

income would be $50,000 and 7.5%

of that amount would be $3,750.

If your medical expenses totaled

$5,000, you would be able to deduct

$1,250 for medical ($5,000 - $3,750).

In the same example, if your medical

expenses were less than $3,750,

there would be no deduction allowed

and no need to list the medical

expenses on your tax return.

|

|

|

|

|

Health

Savings Accounts Offer Tax Breaks

At the end of 2003, the President signed

into law the Medicare Act of 2003. One

of the key provisions of that legislation

was the creation of the Health Savings

Account (HSA). Simply described, a Health

Savings Account is a trust account where

tax-deductible contributions can be made

by qualified taxpayers who have high deductible

medical insurance plans. Income earned

on the HSA balance is income-tax-free.

The funds from these accounts are then

used to pay qualified medical expenses

not covered by the medical insurance for

an eligible individual. If these

funds are not used, they roll over year

to year. At age 65, the funds can be used

like a retirement plan (taxable when withdrawn,

but not subject to a withdrawal penalty)

or continue to be saved for future medical

expenses. Since the contribution is an

above-the-line deduction, a taxpayer need

not itemize to take advantage of this

new tax break. The rules discussed here

are applicable to Federal tax returns

and may not apply to your particular state.

|

Eligible Individual The

new law defines an eligible individual

as one who is covered by a high

deductible plan and, while

covered by that high deductible

plan, is not also covered by another

plan that does not have a high deductible.

For purposes of determining if there

is coverage that does not have a

high deductible, the new law allows

certain types of coverage such as

workers compensation, insurance

for a specific condition, dental

care, vision, long-term care and

certain others to be disregarded.

|

|

High

Deductible Plans High deductible

plans are defined as those with

the following deductible amounts:

-Self-only

coverage with an annual deductible

of $1,000 or more and limits on

annual expenses, other than premiums,

required to be paid by the plan

during the year, up to $5,000; or

-

Family coverage with an annual

deductible of $2,000 or more and

limits on annual expenses, other

than premiums, required to be paid

by the plan during the year, up

to $10,000.

|

|

|

Qualified Medical Expenses

Qualified medical expenses that

can be paid from these accounts

are generally defined as those that

would be allowable as a medical

deduction on your tax return.

|

|

Contribution Limits - The

eligibility and contribution amounts

for these accounts are determined

monthly. Therefore, during any month

in which you qualify, you would

be entitled to contribute 1/12 of

the annual limits. For 2004, the

annual limits are the lesser of

the policy annual deductible or:

-$2,600

for single coverage plans,

-

$5,150 for family coverage plans,

and

-

$500 additional for individuals

age 55 or older.

Individuals entitled to benefits

under Medicare and those claimed

as a dependent on another person's

tax return cannot make contributions.

Contributions can be made as late

as the due date of the tax return

without extensions, and contributions

in excess of the allowable amounts

are subject to an annual 6% excise

penalty. If your employer makes

the contributions for you through

a payroll deduction plan, the contributed

amounts are not subject to normal

payroll withholdings such as FICA

and income taxes.

|

| |

Example:

John, a single taxpayer, age 58,

begins a high deductible health

plan with an annual deductible of

$5,000 starting in March of 2004.

We need to determine his maximum

annual contribution limit ($3,100),

which is the smaller of the deductible

amount or $3,100 ($2,600 plus $500

for being over 55). Next, we divide

the annual limit by 12 to determine

the monthly limit, and in Johns

case, it is $258.33 ($3,100/12).

Since John was in a high deductible

health plan for 10 months during

2004, his contribution limit for

2004 would be $2,583.30 ($258.33

x 10). If John were in the 25% tax

bracket, John would realize a tax

savings of $646.

|

|

|

|

|

Medical

Check List

The following is a checklist of medical

expenses. The list is by no means all-inclusive

and some of the deductions listed may

have additional restrictions not included

here. Please call this office with questions

regarding these or other potential medical

deductions.

- Ambulance

- Artificial

Limb

- Artificial

Teeth

- Birth

Control Pills

- Braille

Books and Magazines

- Abortion

- Legal

- Acupuncture

- Alcoholism

- Chiropractor

- Christian

Science Practitioner

- Contact

Lenses

- Crutches

- Dental

Treatment

- Drug

Addiction

- Drugs

- Eyeglasses

- Fertility

Enhancement

- Guide

Dog

- Hearing

Aids

- Hospital

Services

- Impairment-Related

Expenses

- Insurance

Premiums

- Laboratory

Fees

- Laser

Eye Surgery

- Lead-Based

Paint Removal

- Learning

Disability

|

|

|

|

|

|

Medical

Expenses Relating to Adoption

Medical expense payments made by an adopting

parent for medical services rendered to

a child even before the child was placed

in the parent's home are deductible if:

|

The child is a dependent of the

adopting parent when services are

rendered or paid, and

|

|

The expenses are paid by the parent,

or agent, for the medical care of

the child, and

|

|

They are not reimbursement for

expenses by the adoption agency

prior to adoption negotiations,

and

|

|

The expenses are shown to be directly

attributable to the medical care

of the child.

|

Adoptive parents cannot deduct the natural

mother's childbirth expenses.

|

|

|

|

Alcoholism

& Drug Addiction

You can include in medical expenses amounts

you pay for an inpatient's treatment at

a therapeutic center for alcohol or drug

addiction. This includes meals and lodging

provided by the center during treatment.

You can also include in medical expenses

transportation costs you pay to attend

meetings of an Alcoholics Anonymous Club

in your community, if your attendance

is pursuant to medical advice that membership

in the Alcoholics Anonymous Club is necessary

for the treatment of a disease involving

the excessive use of alcoholic liquors.

|

|

|

|

Cosmetic

Surgery

Generally, cosmetic surgery is not a deductible

medical expense. Cosmetic surgery is defined

as any procedure, which is directed at

improving the patient's appearance and

does not meaningfully promote the proper

function of the body or prevent or treat

illness or disease.

However, cosmetic surgery or other similar

procedures can be taken into account as

a medical expense, if the surgery or procedure

is necessary to ameliorate a deformity

arising from or directly-related to a:

- Congenital

abnormality,

- Personal

injury resulting from an accident or

trauma, or

- Disfiguring

disease.

|

|

|

|

Dependents

& Medical Expenses

Medical Dependents - Medical expenses

paid for dependents may be deducted. To

claim these expenses, the person must

have been a dependent either at the time

the medical services were provided, or

at the time the expenses were paid. A

person generally qualifies as a medical

dependent for purposes of the medical

expense deduction if:

- That

person lived with the taxpayer for the

entire year as a member of the household

or is related,

- That

person was a U.S. citizen or resident,

or a resident of Canada or Mexico for

some part of the calendar year in which

the tax year began, and

- The taxpayer

provided over half of that person's

total support for the calendar year.

Medical expenses of any person who is

a dependent may be included, even if

an exemption for him or her cannot be

claimed on the return.

Child of Divorced or

Separated Parents - If either parent

can claim a child as a dependent under

the rules for divorced or separated parents,

each parent can include the medical expenses

he or she pays for the child. This is

true even if the other parent claims the

exemption for the child.

Support Claimed Under

a Multiple Support Agreement - A multiple

support agreement is used when two or

more people provide more than half of

a person's support, but no one alone provides

more than half. Whoever is considered

to have provided more than half of a person's

support under such an agreement can deduct

medical expenses paid.

Any medical expenses paid by others who

joined in the agreement cannot be included

as medical expenses by anyone.

|

|

|

|

Eldercare

Can Be a Medical Deduction

With people living longer, many find themselves

becoming the care provider for elderly

parents, spouses and others who can no

longer live independently. When this happens,

questions always come up regarding the

tax ramifications associated with the

cost of nursing homes or in-home care.

Generally, the entire cost of nursing

homes, homes for the aged, and assisted

living facilities are deductible as a

medical expense, if the primary reason

for the individual being there is for

medical care or the individual is incapable

of self-care. This would include the entire

cost of meals and lodging at the facility.

On the other hand, if the individual is

in the facility primarily for personal

reasons, then only the expenses directly

related to medical care would be deductible

and the meals and lodging would not be

a deductible medical expense.

As an alternative to nursing homes, many

care providers are hiring day help or

live-in employees to provide the needed

care at home. When this is the case, the

services provided by the employees must

be allocated between household chores

and deductible nursing services. To be

deductible, the nursing services need

not be provided by a nurse so long as

the services are the same services that

would normally be provided by a nurse

such as administering medication, bathing,

feeding, dressing etc. If the employee

also provides general housekeeping services,

then the portion of employee's pay attributable

to household chores would not be a deductible

medical expense.

Household employees, like other employees,

are subject to Social Security and Medicare

taxes, and it is the responsibility of

the employer to withhold the employee's

share of these taxes and to pay the employer's

payroll taxes. Special rules for household

employees greatly simplify these payroll

withholding and reporting requirements

and allow the Federal payroll taxes to

be paid annually in conjunction with the

employer's individual 1040 tax return.

Federal income tax withholding is not

required unless both the employer and

the employee agree to withhold income

tax. However, the employer is still required

to issue a W-2 to the employee and file

the form with the Federal government.

A Federal Employer ID Number and a state

ID number must be obtained for reporting

purposes. Most states have special provisions

for reporting and paying state payroll

taxes on an annual basis that are similar

to the Federal reporting requirements.

If you need assistance in setting up a

household payroll, please contact this

office for additional details and filing

requirements.

|

|

|

|

Impairment-Related

Expenses

Amounts paid for special equipment installed

in the home or for improvements may be

included in medical expenses, if their

main purpose is medical care for the taxpayer,

the spouse, or a dependent. The cost of

permanent improvements that increase the

value of the property may be partly included

as a medical expense. The cost of the

improvement is reduced by the increase

in the value of the property. The difference

is a medical expense. If the value of

the property is not increased by the improvement,

the entire cost is included as a medical

expense.

Certain improvements made to accommodate

a home to a taxpayer's disabled condition,

or that of the spouse or dependents who

live with the taxpayer, do not usually

increase the value of the home and the

cost can be included in full as medical

expenses. These improvements include,

but are not limited to, the following

items:

|

Constructing entrance or exit ramps

for the home,

|

|

Widening doorways at entrances

or exits to the home,

|

|

Widening or otherwise modifying

hallways and interior doorways,

|

|

Installing railings, support bars,

or other modifications,

|

|

Lowering or modifying kitchen cabinets

and equipment,

|

|

Moving or modifying electrical

outlets and fixtures,

|

|

Installing porch lifts and other

forms of lifts but generally not

elevators,

|

|

Modifying fire alarms, smoke detectors,

and other warning systems,

|

|

Modifying stairways,

|

|

Adding handrails or grab bars anywhere

(whether or not in bathrooms),

|

|

Modifying hardware on doors,

|

|

Modifying areas in front of entrance

and exit doorways, and

|

|

Grading the ground to provide access

to the residence.

|

Only reasonable costs to

accommodate a home to a disabled condition

are considered medical care. Additional

costs for personal motives, such as for

architectural or aesthetic reasons, are

not medical expenses.

|

|

|

|

Insurance

Premiums

You can include in medical expenses insurance

premiums you pay for policies that cover

medical care. Policies can provide payment

for:

|

Hospitalization, surgical fees,

x-rays, etc.,

|

|

Prescription drugs,

|

|

Adding handrails or grab bars anywhere

(whether or not in bathrooms),

|

|

Modifying hardware on doors,

|

|

Modifying areas in front of entrance

and exit doorways, and

|

|

Grading the ground to provide access

to the residence.

|

Pre-tax dollars

You cannot deduct insurance premiums

paid with pre-tax dollars because the

premiums are not included in your wages.

If you have a policy that provides more

than one kind of payment, you can include

the premiums for the medical care part

of the policy.

Employer-sponsored health insurance

plan

Do not include in your medical any insurance

premiums paid by your employer-sponsored

health insurance plan, unless the premiums

are included in your wages.

Medicare B

Medicare B is a supplemental medical insurance.

Premiums you pay for Medicare B are a

deductible medical expense.

Prepaid insurance premiums

Premiums you pay before you are age 65,

for insurance for medical care for yourself,

your spouse, or your dependents after

you reach age 65, are medical care expenses

in the year paid, if they are:

- Payable

in equal yearly installments, or more

often, and

- Payable

for at least 10 years, or until you

reach age 65 (but not for less than

5 years).

You cannot include premiums you pay

for:

|

Life insurance policies,

|

|

Policies providing payment for

loss of earnings,

|

|

Policies for loss of life, limb,

sight, etc.

|

|

Policies that pay you a guaranteed

amount each week for a stated number

of weeks if you are hospitalized

for sickness or injury, or

|

|

The part of your car insurance

premiums that provides medical insurance

coverage for all persons injured

in or by your car because the part

of the premium for you, your spouse,

and your dependents is not stated

separately from the part of the

premium for medical care of others.

|

|

|

|

|

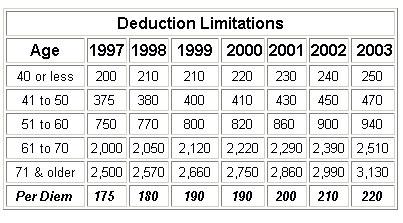

Long-Term

Care

Amounts paid for long-term care services

and certain premiums paid on long-term

care insurance are deductible as medical

expenses on Schedule A. Costs of care

provided by a relative who is not a licensed

professional or by a related corporation

or partnership don't qualify. The maximum

amount of long-term care premiums treated

as medical depends on the insured's age

and is inflation-indexed annually. The

following are the deductible amounts for

the past few years. If the taxpayer paid

long-term care premiums and qualifies

for a medical deduction on Schedule A

of their tax return and did not include

them in their medical deduction, the return

can be amended to include the deduction.

Please call this office to see if the

deduction will make a difference and to

have us prepare the amended returns.

Employees generally won't

be taxed on the value of coverage under

employer-provided long-term care plans.

However, the exclusion doesn't apply if

coverage is provided through a cafeteria

plan. In addition, long-term care services

can't be reimbursed tax-free under a flexible

spending account.

The "Long-term contract" is an

insurance contract that provides only

coverage of long-term care and meets certain

other requirements. Some long-term care

riders to life insurance will also qualify.

Benefits under a long-term care policy

after '96 (other than dividends or premium

refunds) are generally tax-free. For per-diem

contracts that pay a flat-rate benefit

without regard to actual long-term care

expenses incurred, the exclusion is limited

to $175 a day, indexed for medical cost

inflation (amount was $210 in 2002) except

when long-term care costs incurred are

more than the flat rate and are not otherwise

compensated by some other means.

A contract isn't treated

as a qualified long-term care contract

unless the determination of being chronically

ill takes into account at least five activities

of daily living-eating, toileting, transferring,

bathing, dressing and continence.

"Long-term care services" include

necessary diagnostic, preventive, therapeutic,

curing, treating, mitigating, and rehabilitative

services, maintenance or personal care

services prescribed by a licensed practitioner

for the chronically ill.

A "Chronically ill person" is one

who has been certified by a licensed healthcare

practitioner within the previous 12 months

as: (1) unable to perform at least two

activities of daily living (eating, toileting,

transferring, bathing, dressing, continence)

without substantial assistance for a period

of 90 days due to loss of functional capacity,

(2) having a similar level of disability

as determined in regulations, or (3) requiring

substantial supervision to protect from

threats to health and safety due to severe

cognitive impairment. The requirement

that a qualified long-term care insurance

contract must base its determination of

whether an individual is chronically ill

by taking into account five activities

of daily living applies only to (1) above

(being unable to perform at least two

activities of daily living).

|

|

|

|

Medical

Travel Expenses

Auto Travel - Deduction is allowed at

a specified cents per mile rate (see table)

or for actual cost of gas and oil (not

repairs, maintenance, depreciation, lease

fees, etc.)

Trips - Amounts paid

for transportation to another city may

be included in medical expenses, if the

trip is primarily for, and essential to,

receiving medical services. Up to $50

per night for lodging may be included.

A trip or vacation taken merely for a

change in environment, improvement of

morale, or general improvement of health

cannot be included in medical expenses,

even if the trip is made on the advice

of a doctor.

Lodging - The cost of meals and

lodging at a hospital or similar institution

may be included if the main reason for

being there is to receive medical care.

Medical expenses may also include the

cost of lodging not provided in a hospital

or similar institution. The cost of such

lodging while away from home may be included

if all of the following requirements are

met:

- The lodging is primarily for and essential

to medical care.

- The medical care is provided by a

doctor in a licensed hospital or in

a medical care facility related to,

or the equivalent of, a licensed hospital.

- The lodging is not lavish or extravagant

under the circumstances.

- There is no significant element of

personal pleasure, recreation, or vacation

in the travel away from home. The amount

included in medical expenses for lodging

cannot be more than $50 for each night

for each person. Lodging is included

for a person for whom transportation

expenses are a medical expense, because

that person is traveling with the person

receiving the medical care. For example,

if a parent is traveling with a sick

child, up to $100 per night is included

as a medical expense for lodging. Meals

are not deductible.

Meals - Meals are generally not

deductible as a medical expense except

as part of inpatient care. As such, they

would be included in the cost of the hospital

or other medical facility.

|

|

|

| |

|

Nursing

Services

Wages and other amounts paid for nursing

services can be included in medical expenses.

Services need not be performed by a nurse

as long as the services are of a kind

generally performed by a nurse. This includes

services connected with caring for the

patient's condition, such as giving medication

or changing dressings, as well as bathing

and grooming the patient. These services

can be provided in the home or another

care facility.

Generally, only the amount spent for nursing

services is a medical expense. If the

attendant also provides personal and household

services, these amounts must be divided

between the time spent performing household

and personal services and the time spent

for nursing services. However, certain

maintenance or personal care services

provided for qualified long-term care

can be included in medical expenses.

Additionally, certain expenses for household

services or for the care of a qualifying

individual incurred to allow the taxpayer

to work may qualify for the child and

dependent care credit. Part of the amounts

paid for that attendant's meals are also

included in medical expenses. Divide the

food expense among the household members

to find the cost of the attendant's food.

If additional amounts for household upkeep

were paid because of the attendant, include

the extra amounts with the medical expenses.

This includes extra rent or utilities

paid because a larger apartment was needed

to provide space for the attendant.

|

|

|

|

Special

Schools and Education

You can include in medical expenses payments

to a special school for a mentally impaired

or physically disabled person, if the

main reason for using the school is its

resources for relieving the disability.

You can include, for example, the cost

of:

|

Teaching Braille to a visually

impaired child,

|

|

Teaching lip reading to a hearing

impaired child, or

|

|

Giving remedial language training

to correct a condition caused by

a birth defect.

|

The cost of meals, lodging, and ordinary

education supplied by a special school

can be included in medical expenses only

if the main reason for the child's being

there is the resources the school has

for relieving the mental or physical disability.

You cannot include in medical expenses

the cost of sending a problem child to

a special school for benefits the child

may get from the course of study and the

disciplinary methods.

|

|

|

|

Smoke

Cessation Programs

The IRS has ruled that unreimbursed amounts

paid by taxpayers for participation in

smoking-cessation programs and for prescribed

drugs designed to alleviate nicotine withdrawal

are expenses for medical care that are

deductible subject to the 7.5%-of-AGI

limitation. However, because of the prohibition

of deductions for most non-prescription

drugs, no deductions are permitted for

the costs of nonprescription nicotine

gum and certain nicotine patches.

|

|

|

|

Surrogate

Mother Expenses

Surrogate mother expenses are not specifically

addressed in the Tax Code or Regulations.

However, the Code does tell us that medical

expenses are only deductible for the taxpayer,

spouse and dependents. The definition

of a dependent for medical purposes ignores

the gross income and joint return tests.

Therefore, it appears that a surrogate

mother's medical expenses can only be

deducted if she qualifies as a "medical

dependent." The unborn fetus is not a

dependent until actually born.

|

|

|

|

Weight-Loss

Program

Weight-Loss Program The IRS has recently

ruled that expenses for certain weight-loss

programs may be deducted as a medical

expense. In order for uncompensated amounts

paid by individuals for participation

in a weight-loss program to be deductible,

the program must be undertaken as treatment

for a specific disease or diseases (including

obesity) diagnosed by a physician. The

costs are not deductible by taxpayers

who participate in weight-loss programs

to improve their general health or appearance.

Further, the cost of purchasing diet food

items is not deductible.

Prior to this new 2002 ruling, the IRS

took the position that you could only

include in medical expenses the cost of

a weight-loss program undertaken at a

physician's direction to treat an existing

disease (such as heart disease).

This new position affects prior returns

and returns may be amended to claim qualified

expenses. Until April 15th of 2003, the

tax returns for 1999 and later years can

be amended.

|

|

|

|

|

|